MORHomes eyes ‘multitrillion-dollar’ social bond market ahead of debut issuance in new year

MORHomes wants to become a “market disruptor” as it targets a minimum £250m benchmark bond issuance in the new year.

Sharelines

The housing association funding aggregator has a core of 10 borrowers for its maiden deal, and hopes to widen the HA investor base by appealing to a “multitrillion-dollar” impact investment market through its social bond issuer credentials.

Plans for the new funding vehicle – created, owned and run by housing associations – were revealed by Social Housing in June 2017. Its shareholders are housing associations and its model is to leverage the pooled credit of its members to issue bonds via a secured Euro Medium Term Note, which it can then pass on to associations as loans.

A benchmark-size issuance would be well below the £1bn single tranche bond talked about by its founders and directors at the start of the year, and would come at least six months after its intended launch date. The delay has also resulted in a rights issue to raise further funds from its members for running costs, predominantly pre-issue fees.

Patrick Symington, interim chief executive at MORHomes, told Social Housing: “We want to go as soon as we can in the new year and we’re ready to go, but it’s subject to the market.”

He added: “The sector has been absolutely behind this initiative; we have 62 members now, with numbers going up all the time.”

The extra capital from the rights issue means it can “keep going without being up against a deadline”, he added.

The sponsors have already provided an initial £20,000 for shares in the company, taking the initial equity capital to more than £1.2m.

“It’s a sector view that MORHomes is going to be something transformational; a market disruptor,” said Mr Symington.

“It’s quite easy for people to say MORHomes is not proven yet, but what the sector is saying to us is that undoubtedly it’s worth giving it go.”

The structure would accommodate both public and private deals.

Other changes in recent months include the departure of board member Matthew Bailes due to work commitments, and one of the sponsors, Southern Housing Group, has left and issued an own-name bond.

MORHomes has also been in discussions with Homes England and other branches of the UK government about a new wave of financial guarantees, albeit Mr Symington said there is “nothing concrete to report”, adding that the government has “had other priorities”.

Read more

Delays

Mr Symington said the company could have gone to the bond market in November 2018, but did not want to be in a position where it faced the Christmas “rundown of the markets”.

A decision to delay “has been fully vindicated”, with recent issues seeing widening margins and less appetite, he added.

But he conceded: “We have to be honest and say we did slightly underestimate the complexity of going to market, getting our platform built and ready, and getting our borrowers ready.

“That was perhaps a few too many moving parts.

“But the latter two are no longer moving parts; we’ve built the platform and got our core of borrowers, who are committed to borrowing and ready to go, and that will meet our minimum requirement of benchmark size, of £250m-plus.”

That marks a significant climbdown from the £1bn single tranche bond, previously described in February.

Mr Symington said: “Either the markets have moved or we have learned more about it. Very few people issue that size.

“It’s not so much the overall single issue size – and in fact it’s possible £1bn is too much – it’s the repeat issues that is important.”

While he agreed that the UK’s planned departure from the EU “could be a problem”, he pointed to recent fluctuations in gilts, adding: “On the other hand it doesn’t necessarily impact the investors we’re looking at. Brexit doesn’t necessarily mean bad news for HAs going to the market, but if there aren’t investors that’s obviously a problem.”

The recent rights issue dilutes the funding vehicle’s shares, but MORHomes’ shareholders gave the move “almost unanimous” support. Mr Symington would not reveal the figure raised, adding that “although we’re a plc, our shareholding is private”.

He added that while MORHomes is a small team, it has to commit pre-issue costs running into hundreds of thousands if not millions on a potential issue of £0.5bn.

These include advisory, bank and legal costs, which will be spread among the shareholders. Its advisor is JCRA, whose director Adrian Bell helped construct the company, while Allen & Overy and Devonshires are among the legal advisors.

Being different

Asked what makes MORHomes different enough to go beyond the usual six to 10 regular sterling investors in the housing association bond market, Mr Symington said it was a “one stop shop” for investors.

“We’re marketing the sector as a whole,” he said, pointing to global funds that know little about UK housing associations and would not typically spare an analyst to explore it.

“It’s just completely not on their radar, particularly if they are European, Japanese or American,” Mr Symington added.

A unique characteristic is that MORHomes has achieved social bond principles (SBP) set out by the International Capital Market Association (ICMA) as a social bond issuer.

According to JP Morgan, it would become “the first issuer in the UK [of any kind] to issue a social bond which is aligned to the social bond principles”.

Mr Symington said this is one aspect that sets it apart from others in the market and also opens it up to a multitrillion-dollar social bond investment market that seeks an SBP accreditation.

“We’re the only organisation in the UK of any sort to have it for corporate bonds. It seems absolutely extraordinary that the social housing movement hasn’t made more of this because our credentials are unimpeachable; we are social organisations.”

He added: “When it comes down to it, everything MORHomes is doing on the investor side is about widening the market and appeal; repeat issuance, spreading the risk, corporate governance structure, social bond programme, implied government support.”

There is no cross-guarantee between housing associations, and rather than looking at the underlying credit of borrowers the chief executive said MORHomes investors will be looking at the capitalised, corporate structure.

He added: “[Funders] will be investing in MORHomes and won’t even know how the underlying loans are made up, because they don’t need to; they rely on our credit policy and the fact we are spreading our risk across the whole sector.”

By “spreading the risk for investors across the sector”, it can show it can incur 10 per cent of the housing association sector defaulting based on its stress-testing, meaning there would have to be a “complete systemic failure of the whole sector” for investors to lose their money.

Mr Symington would not be drawn on previous claims that the aggregator would achieve a spread of 100 basis points over gilts, adding that “obviously the market has moved; spreads have gone up.”

He pointed to pricing in the secondary markets and the premium associations appear to be paying when compared to other corporates as they are “unknown to the wider pool of investors”.

He added that even the biggest housing association issuers are not issuing to the scale of larger corporates, drawing on the view of board member Malcolm Cooper, who issued around £20bn of debt for National Grid during his time there.

“I can’t give you a view on pricing. You have to talk about it relative to what the rest of the market is doing. But the model is still designed to recapture this price premium, which is in the order of 30-50bps above the equivalents, and we believe that’s achievable.

“It may take more than one issue to get that; to get ourselves established and realise those benefits.”

Enhancement: cost and benefit

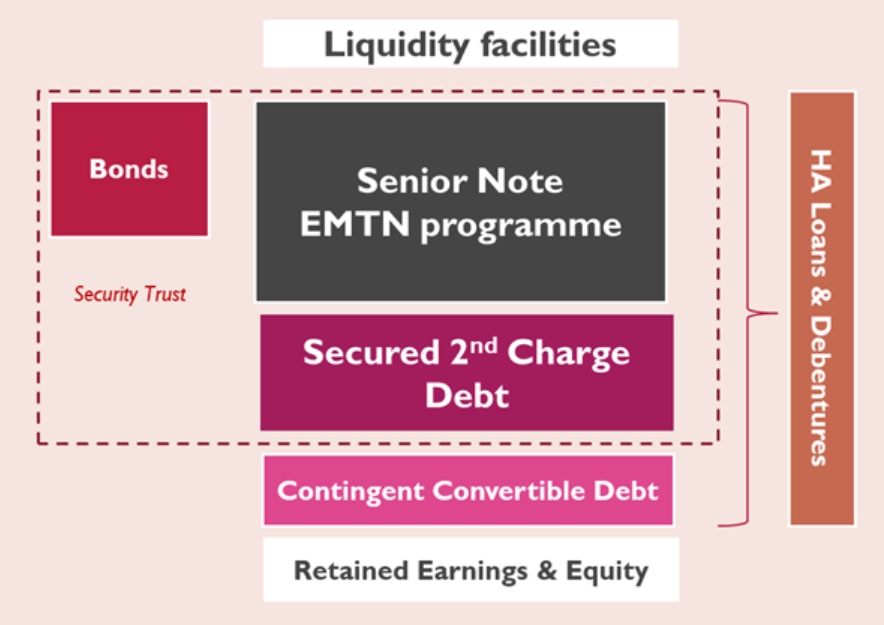

The MORHomes structure has embedded costs for borrowers such as a liquidity facility and the equity investment.

It includes equity and ‘quasi-equity’ in the form of a CoCo – an interest-earning loan from members which is “cash neutral”, according to Mr Symington.

Second secured debt provides a financial buffer and constitutes a note agreement that has been arranged with an investor and will come into play at the time of issuance.

Mr Symington said benefits will include more efficient borrowing, including security charging that can be done within 18 months of the issuance.

Borrowers would also be able to use the funding for whatever purpose they see fit, with no on-lending limits, onerous financial covenants or barriers to investment in commercial activity.

The credit assessment is instead done on the basis of the business plan, meaning they ‘trust’ the association to get it right.

“We take the view that we understand HAs and we credit assess their business plan, and we trust them to manage their finances within the business plan.”

The aggregator is understood to have an A rating from Standard & Poor’s.

Mr Symington said he was unable to publicise the rating until issuance and stressed that it is applied based on the aggregate strength and not the weakest housing association credit. But he added: “It’s not the be-all-and-end-all, is what we’re told; investors will make up their own mind.”

*This story was amended on 18/12/2018 to clarify JCRA’s role as advisor during the creation of MORHomes

RELATED

News10 Mar 2025

Community Housing hires interim chief financial officer

News05 Mar 2025

Two Essex landlords in talks to merge by end of year

funding boost")

- © Social Housing

- All rights reserved