Affordable guarantees gets off mark with £500m loan from EIB

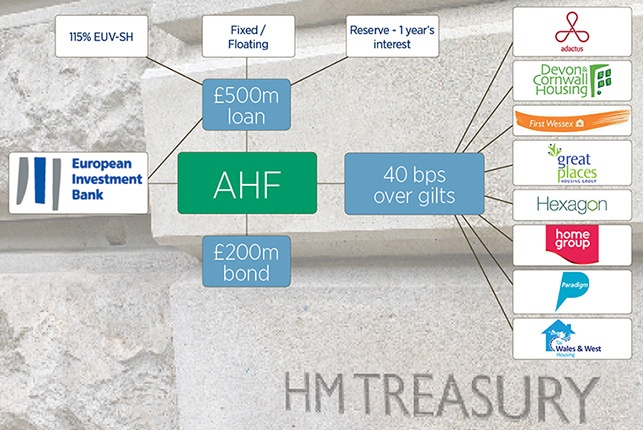

The confirmation of a £500m loan from the European Investment Bank has marked the start of the £3.5bn affordable homes guarantees programme (AHGP).

The programme will see the UK government use its balance sheet to underwrite debt for 30 years with the aim of enhancing credit, lowering borrowing costs and reducing the grant requirement.

Housing minister Kris Hopkins told Social Housing that the EIB loan secured by AHGP delivery partner, Affordable Housing Finance (AHF), represented government ‘opening up new avenues and building new relationships with organisations we have traditionally not explored’, while providing a mechanism for smaller HAs to build.

Eight HAs - First Wessex, Devon and Cornwall Housing (DCH), Paradigm, Home Group, Great Places, Adactus, Wales and West, and Hexagon - have been approved for £400m of debt, which is expected to fund 4,000 new homes.

On closer inspection, however, the structure is more complicated.

The EIB will only fund 50 per cent of the gross value of a development, which means those eight HAs will use part of the EIB funding alongside a share of a proposed £200m ‘splinter’ bond, due to be issued by AHF in April 2014, potentially with AHGP grant from a £450m pot and S106 contributions.

Indicative pricing for the AHGP debt is 40 bps over the reference gilt, which is closer to AAA-rated government-guaranteed Network Rail bonds (32 bps) than any spreads seen in the social housing sector in recent years.

Pricing

There are 20 participants under the AHGP scheme and half of these have been through AHF and Department for Communities and Local Government credit assessments.

The majority of the eight have previously sourced debt via the AHF’s not-for-profit parent, The Housing Finance Corporation, which meant the credit assessments were relatively straight forward, albeit with some additional project-specific queries to meet the requirements of the EIB.

Phil Chisnell, group finance director at Adactus, said the main attraction was cheap funds for a long tenure, with the benefit of THFC and the HA being ‘known quantities’ to each other.

HAs will face an additional 20 bps in administration and arrangement fees, including about 2 bps for the cost of carry on a liquidity reserve, where the EIB requires one year’s interest to be subtracted from the total funds and placed into a holding account.

This still holds up very well against the tightest price in 2013 - a 78 bps margin for Sanctuary’s £150m bond tap, with an A1 Moody’s rating - and is well below the 100 to 150 bps that HAs have tended to secure on the private placement market.

Piers Williamson, chief executive of THFC, said: ‘What comes with this is value for money…it makes scarce resource like grant go even further.’

Any bond pricing however is clearly subject to investor appetite at the time of issue.

Phil Elvy, finance director at Great Places, said: ‘EIB have always been really good on their pricing. For the bond element, it’s difficult to know whether the appetite will really be there, even with a guarantee.

‘THFC have to go away and deliver on that and convince investors to get that much lower return.’

Tony Wilson, finance director at Wales and West, added: ‘You can only look at what alternatives there are in terms of near gilts for some of the issues that have been made on quasi-public sector debt, and therefore it mightbe 60 bps, even 70 bps - but it’s still going to be good value debt.’

Julie Hetherington, treasury manager at Home Group, said they are relying on THFC and their track record, adding: ‘We will just have to see what that is on the day. It’s the risk you take by entering into funding like this.’

Fixed or floating?

The £500m 30-year loan is held by the EIB until HAs decide to draw down, which can be any time until September 2015. It must be taken as a single sum with construction of the underlying affordable projects to start within 12 months.

There is no commitment fee on the EIB loan, which is amortising after 10 years. There are also no corporate covenants.

HAs have the option to borrow fixed or floating debt. If they opt for floating, they can fix after three years or revisit every three years.

A number of the groups intend to use the debt to pay down re-drawable revolving facilities, including Great Places.

Mr Elvy said: ‘Given where the market is and given the only source of long-term funding has been fixed rate long-term, then to take some floating long term makes sense. Otherwise we end up 100 per cent fixed and that’s not the right place to be either.’

Security

The liquidity reserve of one year’s interest is deducted from the funding total and held in trust in an AHF account. Participants do however earn interest on the funds.

Security has been cited by some HAs, particularly in London, as a drawback of AHGP.

It requires a charge of 115% EUV-SH, compared with 105% EUV-SH on recent bonds and private placements, but 150 MV-ST seen under standard THFC terms.

DCLG does not allow for groups to use the market value assessment of their portfolio however, which could arguably enable the sector to draw more money and build more homes.

That reluctance is understood to be due to concerns over residual losses and risk, but is subject to ongoing debate.

Using EUV-SH is ‘not the most efficient use of housing properties’, according to Ms Hetherington, at Home Group.

Of the eight HAs in the programme, few expect their gearing levels to alter by more than a few percentage points.

Projects

Finance under the AHGP can only be used for new build affordable rent and home ownership projects after the 2011-15 grant funding round, with a minimum of £5m

of funding.

The HCA has allocated £220m to 69 providers as part of a £450m pot of grant available under AHGP to deliver 30,000 homes, which can be taken exclusively from the debt.

Half of the HAs approved for the first tranches of AHGP debt did not receive any grant under the programme.

All eight groups said they will predominately build houses with a smaller proportion of flats, while also incorporating 10 to 20 per cent of shared ownership properties into their sites.

The EIB does not fund the shared ownership properties and will not fund land costs.

Affordable rent levels vary, with a number of groups saying they plan to charge 80 per cent of market rent.

Wales and West HG’s guaranteed funding is tied in with the £130m Welsh Housing Finance Grant (WHFG), under which the AHF plans to provide £35m of debt.

A £4m per annum, 30-year revenue subsidy form the Welsh Government underpins the WHFG.

What’s next

Mr Williamson is expecting more housing providers to come forward now the first deals are in motion, and agreed there are likely to be HAs looking at the scheme now they are clearer on the post-2015 grant funding round.

AHF is set to return to the EIB for a second tranche of debt, but there is still some way to go to reach the £3.5bn ceiling.

AHGP will be extended by a year, taking the contract with AHF to March 2016.

The EIB said it is looking forward to ‘further engagement’ with the sector in the coming months.

It is planning to lend directly to some of the largest HAs in the UK and has approved in principle a £350m bilateral loan facility to Sanctuary, with documentation nearing completion and hopes for sign-off before the end of the financial year.

Eleven HAs are also in line for around £400m of ‘eco funding’ from the EIB, which requires attaining Code for Sustainable Homes standard levels 4. Family Mosaic secured £50m at 3.91 per cent over 30 years, amortising after year 10, which means an average life of 20 years.

While the EIB has traditionally required projects to meet urban regeneration criteria, Jonathan Taylor, EIB vice president responsible for the UK, said it is now broadening its focus.

‘We started off with a slightly narrower focus. It’s not a change but an addition and broadening [of] our scope.’

Mr Hopkins added: ‘I think there is a change going on in the way the social rented market is perceived; [this is] high quality provision which is sustainable and which is attracting international investment into this market.’

Read more

Related Files

Affordable homes guarantees programmePDF, 1.4 MB

RELATED

News11 Mar 2025

Platform doubles EMTN programme capacity to £2bn

Comment11 Mar 2025

It is time for a new chapter on social housing finance

News10 Mar 2025

Community Housing hires interim chief financial officer

- © Social Housing

- All rights reserved